Fourth, the controls won’t be nearly enough. Even if the Europeans could prevent capital from leaving, raising capital to fund emergency spending the old-fashioned way isn’t as quick or effective as the American method of simply flipping the switch on the printing press. Firms would fold in the thousands, and the damage will not be limited to the small players. To stave off the subsequent economic and cultural carnage, expect mass nationalizations throughout European economies. Unsurprisingly, the French are already discussing the mechanics of how to manage this. Peugeot, Renault and Airbus have already indicated they will fight the process (although they’d still love help with recapitalization and operating costs).

Fifth, this is likely the end of “European” manufacturing. The European manufacturing system, especially the German manufacturing system, is based on the free movement of goods, people and capital across borders. That simply isn’t possible in an environment of national quarantine, capital flight, capital controls and nationalizations. Post-crisis things will still be made in Germany and Bulgaria and Sweden and so on, but not all that much is likely to be the result of a multi-national European supply chain.

This is doubly problematic in the short term as most European countries lack even small pieces of the medical supply chain. While the US can retool and China can get back to work, many European states simply don’t have

anythingwithin their borders they can use.

The dream of Europe was that open borders would enable Europe to have economies of scale of the Chinese or American type. But these are still separate countries, and the utter inability of the EU to ride to the rescue leaves individual states more or less on their own at the worst possible time. Germany, for one, is a major exporter of medical equipment, and it has already barred exports of many coronavirus-related materials. Even to its EU partners. Many Europeans already resent Germans’ unwillingness to share their wealth. Imagine how refusal to share medical equipment will go over once the death toll gets seriously scary.

Sixth, this is the end of the European economic and social model, and it risks being the end of “Europe” as an entity.

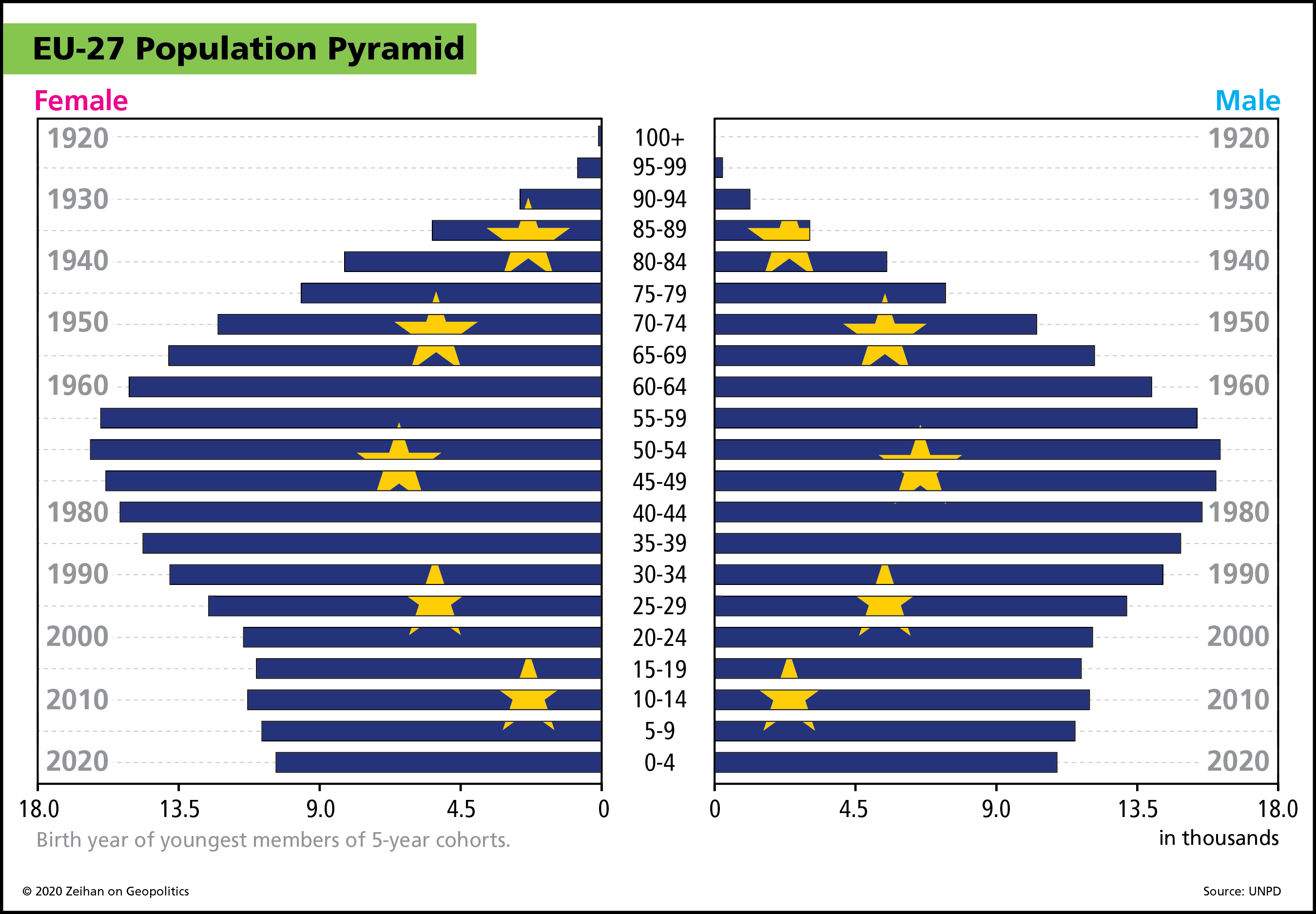

- Europe’s demographics make consumption-led growth impossible, even as coronavirus blocks export-led growth.

- The Americans were backing away from the global security rubric that makes Europe’s export-led growth model possiblebeforecoronavirus, and the virus is only accelerating America’s turning-inward.

- Europe lacks the institutional capacity to manage crisis response.

- Europe lacks the financial capacity to cope with the crisis, much less apply the sort of financial fire-hose the Americans did almost reflexively.

- Dealing with the virus’ spread has already forced the Europeans to abandon the free movement of people.

- Dealing with their financial shortfalls will force them to abandon the free movement of capital.

- Dealing with mass nationalizations and the loss of export markets will force them to abandon the free movement of goods.

That’s three of the four freedoms upon which modern Europe relies. The fourth freedom – movement of services – was largely something that only the UK cared about, and the Brits are gone.

There is one possible “solution” to these problems: drop the euro.

If the Maastricht Treaty were abrogated (or at least suspended) and national control over monetary policy reintroduced, individual European countries could then engage in unlimited quantitative easing, both to mitigate the current crisis and to help manage the subsequent damage and recovery. This would (obviously) hold (many) downsides, but if the goal is to have the necessary capital required to address the current crisis, this is the only path I see that still results in salvaging Europe’s current economic and social structure.

In theory, once coronavirus was in the rear-view mirror, Europe could go through the process of re-merging their currencies (perhaps this time without basket cases like Greece). Yes, I realize this would be monumentally messy, but we’re already in a world where economic and financial norms are in abeyance. Most of contemporary Europe’s “messes” require extensive multi-national negations. This “plan” has the advantage of countries doing things themselves.

Regardless of the path forward (or down) coronavirus is just the beginning of Europe’s problems. Demographics, economics, financials, supply chains, none of it works under coronavirus – and coronavirus is going to be with us until we either get a vaccine, herd immunity or mass serological testing, none of which is particularly likely to happen in 2020. Even then, it is far from clear that Europe has we know it can reconstitute in the world after coronavirus. And never forget that all Europe is not created equal. Germany is not France is not Italy is not Poland is not Sweden is not Portugal is not Romania.

An end to the concept of “European” being singular represents more than simply the return to the norm of European history, it removes one of the central pillars of the world we know. That cascading failure and the reordering to come will be a subject in subsequent installments in our Coronavirus Guides series.